Mortgage in Morocco: the conditions offered by banks in 2026

mortgage in morocco: the conditions offered by banks in 2026

24 February 2026

REAL-DREAMHOUSE | Real Estate Blog | February 2026

Are you considering buying a property in Morocco in 2026? Good news: the mortgage market is going through a period of stabilization favorable to buyers. Competitive rates, government aid, digitization of procedures... Here is a comprehensive overview of the conditions offered by the main Moroccan banks this year.

1. The context: a stabilized market after turbulence

After an adjustment phase in 2025, the mortgage market in Morocco is moving in 2026 into a stabilization phase. Bank Al-Maghrib has maintained its key rate at 2.25%, a level that continues to support attractive borrowing conditions for households and investors.

Also worth noting: the "2030 World Cup" effect is beginning to be felt on Moroccan land values, with a gradual revaluation of areas close to future infrastructure — stadiums, LGV stations, upscale hotels. Buying now also means anticipating a potential rise in prices over the coming years.

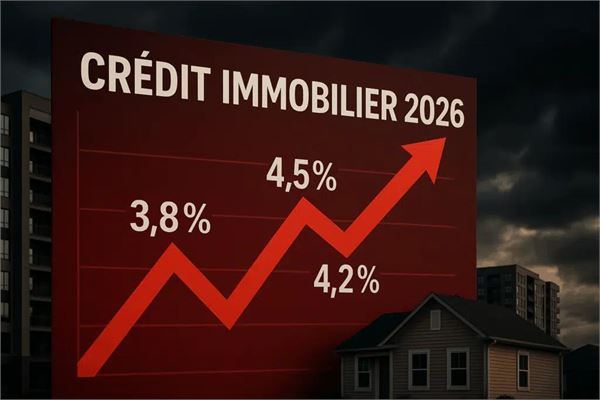

2. Rates in 2026: what banks are offering

At the start of 2026, borrowing rates (excluding taxes, excluding insurance) generally range between 4,10% and 5,20% depending on the institution, the borrower's profile, and the loan term.

Indicative comparison of the main banks:

Bank Fixed rate Variable rate Max term

Attijariwafa Bank 4,50% – 5,00% 4,20% – 4,80% 25 years

Banque Populaire 4,60% – 5,10% 4,30% – 4,90% 25 years

CIH Bank 4,40% – 4,90% 4,10% – 4,70% 25 years

BMCE / Bank of Africa 4,50% – 5,20% 4,20% – 4,90% 27 years

BMCI 4,50% – 5,10% Annual variable 25 years

Société Générale Morocco 4,60% – 5,00% 4,30% – 4,80% 25 years

⚠️ Indicative rates excluding insurance. Differences of 0,20% to 0,50% are negotiable depending on your profile.

3. Who can borrow? Access conditions by profile

Conditions vary significantly depending on your situation:

Private and public sector employees

Financing up to 90% of the property's price (sometimes 100% for civil servants)

Term up to 25 years

Permitted debt-to-income ratio: 45% for income up to 20 000 DH/month, 50% beyond

Down payment: generally a minimum of 10%

Business owners and self-employed

Required down payment between 20% and 30%

Enhanced financial file (balance sheets, tax returns over 3 years)

Slightly higher rates depending on the strength of the profile

Moroccans Residing Abroad (MRE)

Financing up to 70–80% of the property's amount

Systematic down payment between 10% and 50% depending on the institution

100% digitized procedures facilitating remote processes

Accounts in convertible dirhams or in foreign currencies accepted

4. Murabaha: a booming Islamic alternative

Since 2017, participatory banks (Umnia Bank, CIH Dar, Al Akhdar Bank) have been offering solutions compliant with the principles of Islamic finance. The real estate Murabaha contract works as follows: the bank buys the property on your behalf and then sells it back to you at a price increased by a transparent profit margin, with no interest.

In 2026, these offers appeal to a growing number of borrowers, both for religious convictions and for the total clarity of the financial arrangement. The total amount to be repaid is fixed from the outset — no nasty surprises.

5. Insurance: the hidden cost you must not overlook

Often relegated to the background, death-disability insurance nevertheless weighs heavily on the total cost of your loan. In 2026, the average rate is around 0,43% of the capital borrowed per year.

Good news: you're not required to take your bank's insurance. Delegated insurance allows you to choose an external insurer that is often more competitive. A loan at 4,20% with optimized insurance can therefore end up costing less than a loan at 3,90% with standard bank insurance.

6. A concrete example: how much can you save by negotiating?

For a 500 000 MAD loan over 25 years, here's what a rate gap represents:

Applied rate Monthly payment Total cost Savings vs 5,10%

5,10% ≈ 3 247 MAD ≈ 974 000 MAD —

4,50% ≈ 3 057 MAD ≈ 917 000 MAD 57 000 MAD

4,10% ≈ 2 943 MAD ≈ 883 000 MAD 91 000 MAD

Half a percentage point negotiated can sometimes amount to several years of payments saved. It's well worth the time spent comparing offers.

7. Our 5 tips to get the best financing in 2026

1. Shop around Never settle for your usual bank's offer. Approach at least 3 different institutions. A mortgage broker can save you between 0,20% and 0,50% on your rate.

2. Polish your file Bank statements for the last 6 months, proof of income, stable professional situation: a strong file is your best bargaining chip. Banks favor predictable profiles.

3. Optimize your debt ratio Keep your ratio below 45% for standard incomes. Pay off your consumer loans before submitting your application if possible.

4. Don't overlook ancillary fees Application fees (0,3% to 1% of the amount), mortgage, insurance, notary and land registry fees: all these elements add up. Negotiate them as well; some are reducible.

5. Find out about the Daam Sakan aid If you're a first-time buyer, check your eligibility for direct government aid even before you start looking for your property. This program can significantly reduce your required down payment.

Conclusion: 2026, a window of opportunity to seize

The Moroccan mortgage market in 2026 offers a rare combination: rates stabilized at competitive levels, digitized procedures that make the process easier, and momentum driven by anticipation of the 2030 World Cup.

Whether you are a resident, an MRE, a first-time buyer, or an investor, there is a financing solution suited to your profile. The challenge is no longer to wait for a hypothetical rate cut, but to optimize the overall conditions of your financing starting today.

📞 Do you have a real estate project in Morocco? Contact our Real-dreamHouse advisors for a free, personalized simulation. www.real-dreamhouse.comREAL-DREAMHOUSE | Real Estate Blog | February 2026

Are you considering buying a property in Morocco in 2026? Good news: the mortgage market is going through a period of stabilization favorable to buyers. Competitive rates, government aid, digitization of procedures... Here is a comprehensive overview of the conditions offered by the main Moroccan banks this year.

1. The context: a stabilized market after turbulence

After an adjustment phase in 2025, the mortgage market in Morocco is moving in 2026 into a stabilization phase. Bank Al-Maghrib has maintained its key rate at 2.25%, a level that continues to support attractive borrowing conditions for households and investors.

Also worth noting: the "2030 World Cup" effect is beginning to be felt on Moroccan land values, with a gradual revaluation of areas close to future infrastructure — stadiums, LGV stations, upscale hotels. Buying now also means anticipating a potential rise in prices over the coming years.

2. Rates in 2026: what banks are offering

At the start of 2026, borrowing rates (excluding taxes, excluding insurance) generally range between 4,10% and 5,20% depending on the institution, the borrower's profile, and the loan term.

Indicative comparison of the main banks:

Bank Fixed rate Variable rate Max term

Attijariwafa Bank 4,50% – 5,00% 4,20% – 4,80% 25 years

Banque Populaire 4,60% – 5,10% 4,30% – 4,90% 25 years

CIH Bank 4,40% – 4,90% 4,10% – 4,70% 25 years

BMCE / Bank of Africa 4,50% – 5,20% 4,20% – 4,90% 27 years

BMCI 4,50% – 5,10% Annual variable 25 years

Société Générale Morocco 4,60% – 5,00% 4,30% – 4,80% 25 years

⚠️ Indicative rates excluding insurance. Differences of 0,20% to 0,50% are negotiable depending on your profile.

3. Who can borrow? Access conditions by profile

Conditions vary significantly depending on your situation:

Private and public sector employees

Financing up to 90% of the property's price (sometimes 100% for civil servants)

Term up to 25 years

Permitted debt-to-income ratio: 45% for income up to 20 000 DH/month, 50% beyond

Down payment: generally a minimum of 10%

Business owners and self-employed

Required down payment between 20% and 30%

Enhanced financial file (balance sheets, tax returns over 3 years)

Slightly higher rates depending on the strength of the profile

Moroccans Residing Abroad (MRE)

Financing up to 70–80% of the property's amount

Systematic down payment between 10% and 50% depending on the institution

100% digitized procedures facilitating remote processes

Accounts in convertible dirhams or in foreign currencies accepted

4. Murabaha: a booming Islamic alternative

Since 2017, participatory banks (Umnia Bank, CIH Dar, Al Akhdar Bank) have been offering solutions compliant with the principles of Islamic finance. The real estate Murabaha contract works as follows: the bank buys the property on your behalf and then sells it back to you at a price increased by a transparent profit margin, with no interest.

In 2026, these offers appeal to a growing number of borrowers, both for religious convictions and for the total clarity of the financial arrangement. The total amount to be repaid is fixed from the outset — no nasty surprises.

5. Insurance: the hidden cost you must not overlook

Often relegated to the background, death-disability insurance nevertheless weighs heavily on the total cost of your loan. In 2026, the average rate is around 0,43% of the capital borrowed per year.

Good news: you're not required to take your bank's insurance. Delegated insurance allows you to choose an external insurer that is often more competitive. A loan at 4,20% with optimized insurance can therefore end up costing less than a loan at 3,90% with standard bank insurance.

6. A concrete example: how much can you save by negotiating?

For a 500 000 MAD loan over 25 years, here's what a rate gap represents:

Applied rate Monthly payment Total cost Savings vs 5,10%

5,10% ≈ 3 247 MAD ≈ 974 000 MAD —

4,50% ≈ 3 057 MAD ≈ 917 000 MAD 57 000 MAD

4,10% ≈ 2 943 MAD ≈ 883 000 MAD 91 000 MAD

Half a percentage point negotiated can sometimes amount to several years of payments saved. It's well worth the time spent comparing offers.

7. Our 5 tips to get the best financing in 2026

1. Shop around Never settle for your usual bank's offer. Approach at least 3 different institutions. A mortgage broker can save you between 0,20% and 0,50% on your rate.

2. Polish your file Bank statements for the last 6 months, proof of income, stable professional situation: a strong file is your best bargaining chip. Banks favor predictable profiles.

3. Optimize your debt ratio Keep your ratio below 45% for standard incomes. Pay off your consumer loans before submitting your application if possible.

4. Don't overlook ancillary fees Application fees (0,3% to 1% of the amount), mortgage, insurance, notary and land registry fees: all these elements add up. Negotiate them as well; some are reducible.

5. Find out about the Daam Sakan aid If you're a first-time buyer, check your eligibility for direct government aid even before you start looking for your property. This program can significantly reduce your required down payment.

Conclusion: 2026, a window of opportunity to seize

The Moroccan mortgage market in 2026 offers a rare combination: rates stabilized at competitive levels, digitized procedures that make the process easier, and momentum driven by anticipation of the 2030 World Cup.

Whether you are a resident, an MRE, a first-time buyer, or an investor, there is a financing solution suited to your profile. The challenge is no longer to wait for a hypothetical rate cut, but to optimize the overall conditions of your financing starting today.

📞 Do you have a real estate project in Morocco? Contact our Real-dreamHouse advisors for a free, personalized simulation. www.real-dreamhouse.com

L'équipe de Real-dreamhouse

Notre équipe dynamique et dédiée à la clé de votre succès. Nous offrons un service professionnel sur mesure, respectant des standards élevés pour réaliser vos ambitions immobilières.

Benoit PRIVEL

Fondateur Manager

Salwa SAMSAK

Manager Événementiel

Sophie BELLAVOINE

Manager Consultant

Tawfik BOUAMANE

Consultant Manager RabatContact us for a free valuation of your property!

Get a free and reliable valuation of your property in Marrakech, carried out by our local experts.